AI gives, AI takes: the new physics of non-physical businesses

Mapping which businesses will win, where, and why.

AI is changing the physics of non-physical businesses. It turns labor into compute, workflow into automation, and expertise into a scalable capability. That doesn't just create new products — it rewires margins, pricing power, defensibility, and distribution across software, services, media, research, and operations.

AI gives productivity, speed, and personalization — and lowers the marginal cost of delivering outcomes.

AI takes seat-based pricing power, challenges billable-hour models, and weakens defensibility built on feature sets.

For builders and investors, it’s no longer whether a company is an AI company; that question is outdated. A better one is: what company are you becoming as AI changes cost, pricing, and distribution? Where is your default gravity — where do you win first?

Default gravity — the segment where your offering faces the least distribution friction and the unit economics work best, making it the most likely place to win first and compound value.

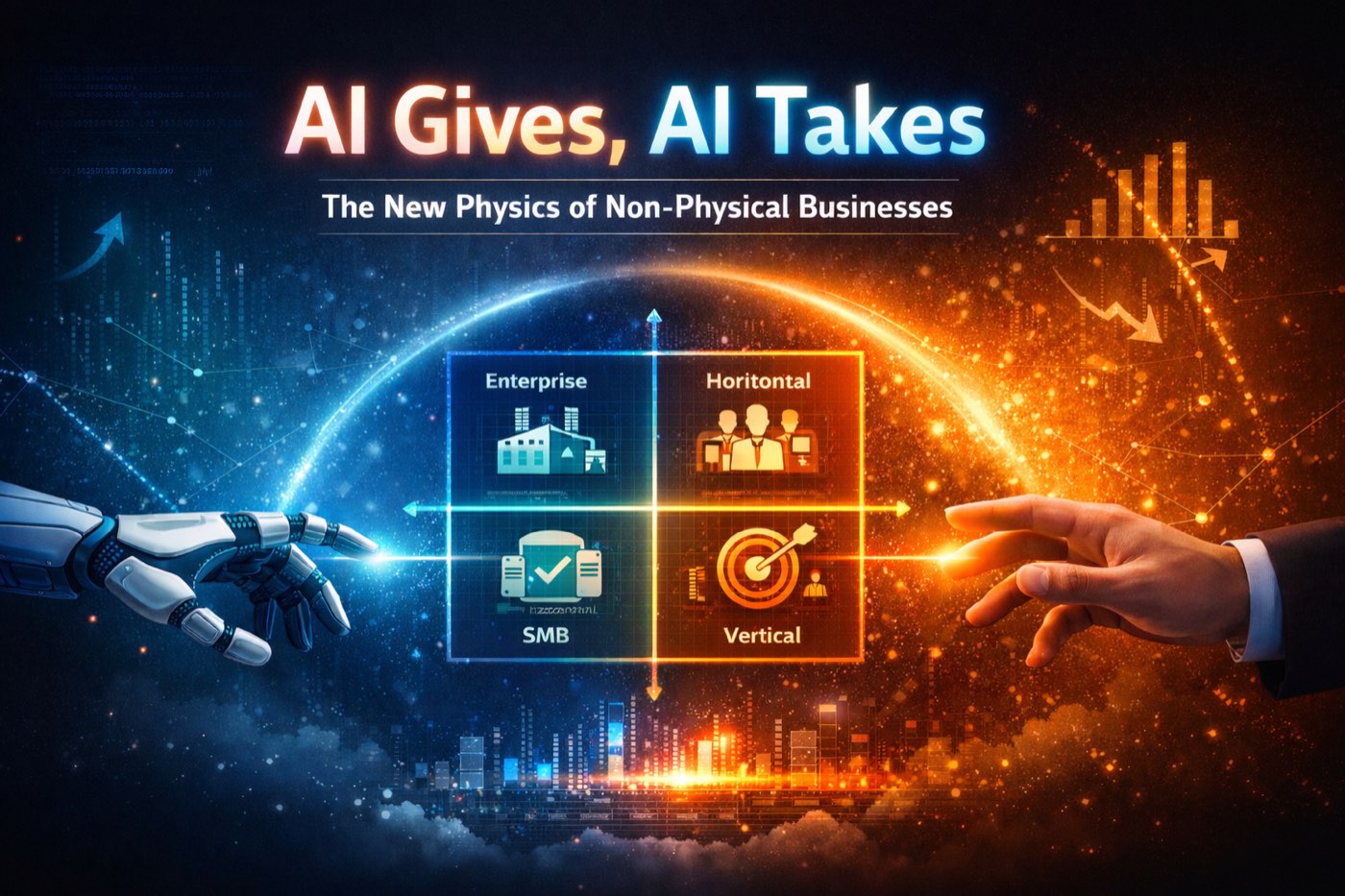

This piece uses a simple framework: five AI archetypes on a 2×2 grid to help you choose where and how to compete. There will be exceptions; we focus on the primary winners in each quadrant.

The 2×2 gravity map

X-axis: Horizontal ↔ Vertical

- Horizontal — broad primitives across industries (productivity, search, workflow, analytics, orchestration, security).

- Vertical — domain-specific workflows with embedded context (claims, clinical ops, construction change orders, underwriting, close, compliance, and so on).

Rule of thumb: horizontal wins on repeatability; vertical wins on context.

Y-axis: Enterprise ↔ SMB

- Enterprise — integration-heavy, audit-heavy, slow procurement, high trust and liability requirements.

- SMB — speed of adoption, packaged value, price sensitivity, lower tolerance for complexity.

Rule of thumb: enterprise rewards governance and credibility; SMB rewards time-to-value and packaging.

The AI Gravity Map — where each archetype’s gravity pulls it to win first:

| Segment | Horizontal | Vertical |

|---|---|---|

| Enterprise | SaaS_Incumbent.AI |

Services_Incumbent.AIAI-native_SaaS (enterprise play) |

| SMB | AI-native_SaaS (SMB play) |

AI-native_ServicesSaaS_Outcome.AI |

Now let’s define each archetype, why it exists, and why gravity pulls it where it does.

Archetype 1: Services_Incumbent.AI

Existing services firms transforming delivery with AI.

What it is. A services incumbent — an agency, consultancy, law or accounting firm, BPO, or IT services provider — uses AI to improve labor efficiency, speed, quality, and margins while maintaining core service relationships. This archetype is distinct in its focus on adapting existing service models through AI, rather than creating entirely new offerings.

Why it exists. These firms already possess customer trust and manage complex workflows. AI introduces a significant productivity boost rather than creating a new product category.

Default gravity: Enterprise + Vertical. Incumbents hold a natural advantage here:

- Trust and liability matter.

- Exceptions are everywhere.

- Human sign-off is required (regulation, risk, brand).

Where they win

- Installed relationships and procurement access.

- Deep domain expertise and edge-case handling.

- Credibility in regulated environments.

- The ability to wrap AI into an existing “outcome promise.”

Where they feel pressure

- Cannibalization — AI reduces billable hours; culture fights efficiency.

- Incentive misalignment — utilization models resist productization.

- AI-native challengers with cleaner packaging and faster iteration.

- Pricing compression without volume expansion if they don’t change the go-to-market motion.

Where economics tend to settle. This archetype often evolves into a hybrid model with improved margins and faster delivery. But it doesn’t become “SaaS-like” unless services are productized into recurring bundles. The key is not simply adding more AI, but repackaging delivery into repeatable products. Over time, many niches consolidate as leading operators combine trust with AI-driven efficiency — expect oligopoly per vertical rather than winner-take-all.

Archetype 2: AI-native_Services

New AI-native companies selling the outcome directly.

What it is. A new company that delivers finished work using AI-driven workflow automation, with humans only for exceptions or QC. Unlike incumbents, these companies build their operations and customer engagement directly around AI, not people.

Why it exists. AI reduces outcome-delivery costs, enabling scalable, outcome-based solutions in labor-intensive markets.

Default gravity: SMB + Vertical. That’s where outcome products wedge fastest:

- Narrow, repeatable workflows.

- Clear pain.

- Willingness to buy a packaged “done-for-you.”

- Faster sales cycles, fewer gatekeepers.

Where they win

- Clean packaging from day one (subscription / outcome bundles).

- Faster iteration loops (product DNA, not services DNA).

- A compounding advantage if they capture domain feedback and exceptions as “product learning.”

- A price-performance discontinuity for SMB buyers.

Where they feel pressure

- Trust deficit — buyers are skeptical when software “does the work.”

- Exception creep — too many edge cases turn it into disguised services.

- Compliance and audit requirements as they move upmarket.

- A distribution disadvantage versus incumbents with existing relationships.

Where economics tend to settle. If exception handling stays manageable, software-like margins and scalability follow. If not, the model reverts to services. The key metric: the percentage of volume handled end-to-end without human escalation.

Archetype 3: SaaS_Incumbent.AI

Existing SaaS companies adding AI capabilities.

What it is. An established SaaS provider that adds AI features — copilots, agents, automation — to existing offerings. Unlike AI-native SaaS, these companies retrofit AI into software built for pre-AI workflows and customer relationships.

Why it exists. Incumbent SaaS providers control distribution, data context, and workflow surface area — all essential for maximizing AI’s value.

Default gravity: Enterprise + Horizontal. This is the natural domain of SaaS incumbents because:

- Their value is broad workflow enablement.

- Enterprise buyers already trust them with systems of record and audit trails.

- The upsell path is native: “pay more, get automation.”

Where they win

- Installed base and low-friction upsell.

- Workflow gravity and user habituation.

- Context (permissions, audit logs, historical data).

- Procurement clearance and security posture.

Where they feel pressure

- Unbundling risk from horizontal agent platforms that reduce the need for point tools.

- Pricing pressure as AI collapses seat-based value perception.

- Execution debt — legacy architecture slows agent-native redesign.

- Feature parity — AI “features” become table stakes quickly.

Where economics tend to settle. Resilient in the short term — AI can be monetized without reinventing distribution. The medium-term question is whether they remain “tools + features” or become orchestrators that own end-to-end automation.

Archetype 4: AI-native_SaaS

AI-native software companies — or AI apps — where AI is the product.

What it is. AI-first software companies that sell software, but where AI is the primary value engine: generation, reasoning, retrieval, orchestration, decision support, and automation.

Why it exists. Some tasks are universal enough to support horizontal products; others require deep context, making enterprise vertical workflows the most effective route to lasting value.

Default gravity: two winners — Horizontal + SMB, and Enterprise + Vertical. This split is not a contradiction; it’s how AI markets actually form.

Gravity point A — Horizontal + SMB. SMB rewards immediate value, self-serve adoption, and tools that work without integration projects. Where they win: speed, product-led growth, broad TAM, low onboarding friction. Where they feel pressure: churn, commoditization, and platform absorption if they don’t build a moat.

Gravity point B — Enterprise + Vertical. Enterprise vertical rewards measurable ROI, workflow ownership, governance and compliance, and integration depth (AI becomes system behavior, not a feature). Where they win: high-value workflows automated inside domain constraints. Where they feel pressure: long sales cycles, audits, liability, and the need to prove reliability over time.

Where economics tend to settle. Horizontal + SMB versions scale quickly but face churn and feature parity. Enterprise + vertical versions grow more slowly but can become durable if they own the workflow and build a data flywheel.

Archetype 5: SaaS_Outcome.AI

SaaS companies moving from “tools” to “done-for-you outcomes.”

What it is. A vertical SaaS provider that transitions from being only a software tool to providing a fully managed, outcome-oriented service powered by AI. This archetype differs from traditional SaaS by handling more of the user’s workflow end-to-end.

Why it exists. Vertical SaaS is already embedded in operational workflows. The most direct route to AI value is not additional dashboards, but automation that completes the workflow.

Default gravity: SMB + Vertical. SMB is the natural initial landing zone because:

- SMB buyers want outcomes, not configuration.

- They’ll pay for “done-for-you” packaged tiers.

- The implementation burden must be low — and vertical SaaS can deliver within its own workflow.

Where they win

- Built-in distribution and workflow ownership.

- Native context (data model, history, permissions).

- A packaging advantage: premium tiers, bundles, predictable subscriptions.

- Strong retention potential if the outcome is mission-critical.

Where they feel pressure

- Margin dilution if humans creep into delivery (the managed-services trap).

- Support burden if customer workflows are messy and non-standard.

- Accountability expansion — once you own the outcome, you inherit its failure modes.

- Operational maturity — outcome delivery requires QA, controls, and incident response.

Where economics tend to settle. This archetype can reach significant scale if the service layer stays automation-focused and exceptions are tightly controlled. Done well, it materially increases average contract value and retention. Done poorly, it may still grow fast — but with different margin and valuation expectations.

Implications for the coming decade

The first wave of clear winners will be those with strong distribution. The fastest compounding advantage in AI is not model quality — it’s proprietary usage loops. The channel that gives you rapid adoption and unique feedback data becomes your defensibility.

The biggest long-term upside concentrates where outcome ownership meets workflow context. SaaS won by understanding workflows and locking information into a system of record. AI wins by understanding context and unlocking intelligence as the system of intelligence.

AI-native_SaaS splits into two separate games. In SMB horizontal: win distribution, defend against commoditization. In enterprise vertical: win workflow, defend with governance and data.

Gravity isn’t destiny — but it is your starting battlefield. If your product and go-to-market don’t match your quadrant’s buying physics, the market will punish you.

The practical takeaway: pick your archetype on purpose

If you’re building tools, your moat must be deeper than “AI UX” — think control planes, governance, and embedded distribution.

If you’re building outcomes, your moat must be deeper than “model quality” — prioritize exception handling, reliability, workflow ownership, and data compounding.

And if you’re scaling:

- Enterprise rewards trust architecture.

- SMB rewards packaging architecture.

- Horizontal rewards distribution architecture.

- Vertical rewards context architecture.

That’s the new physics. Not “AI vs SaaS.” Not “agents replace apps.” AI gives some, takes some. Whether you work with or against the gravitational pull of your quadrant decides who wins first.

Related questions

- What does 'default gravity' mean for an AI business?

- Default gravity is the segment where your offering faces the least distribution friction and the unit economics work best — making it the most likely place to win first and compound value. It is your starting battlefield, not your destiny: if your product and go-to-market don't match your quadrant's buying physics, the market punishes you.

- What are the five AI business archetypes?

- Services_Incumbent.AI (existing services firms using AI to improve delivery), AI-native_Services (new firms selling the finished outcome directly), SaaS_Incumbent.AI (established SaaS adding AI features), AI-native_SaaS (AI-first software where AI is the primary value engine), and SaaS_Outcome.AI (vertical SaaS moving from tools to done-for-you outcomes).

- Does AI replace SaaS?

- No. The framing 'AI vs SaaS' or 'agents replace apps' is the wrong one. AI gives some things — productivity, speed, personalization, and lower marginal cost — and takes others — seat-based pricing power, billable-hour models, and feature-based defensibility. Whether you work with or against the gravitational pull of your quadrant decides who wins first.