The price didn't change. Your bill did.

The stealth inflation in AI software that no price tracker catches — because the number on the pricing page never moves.

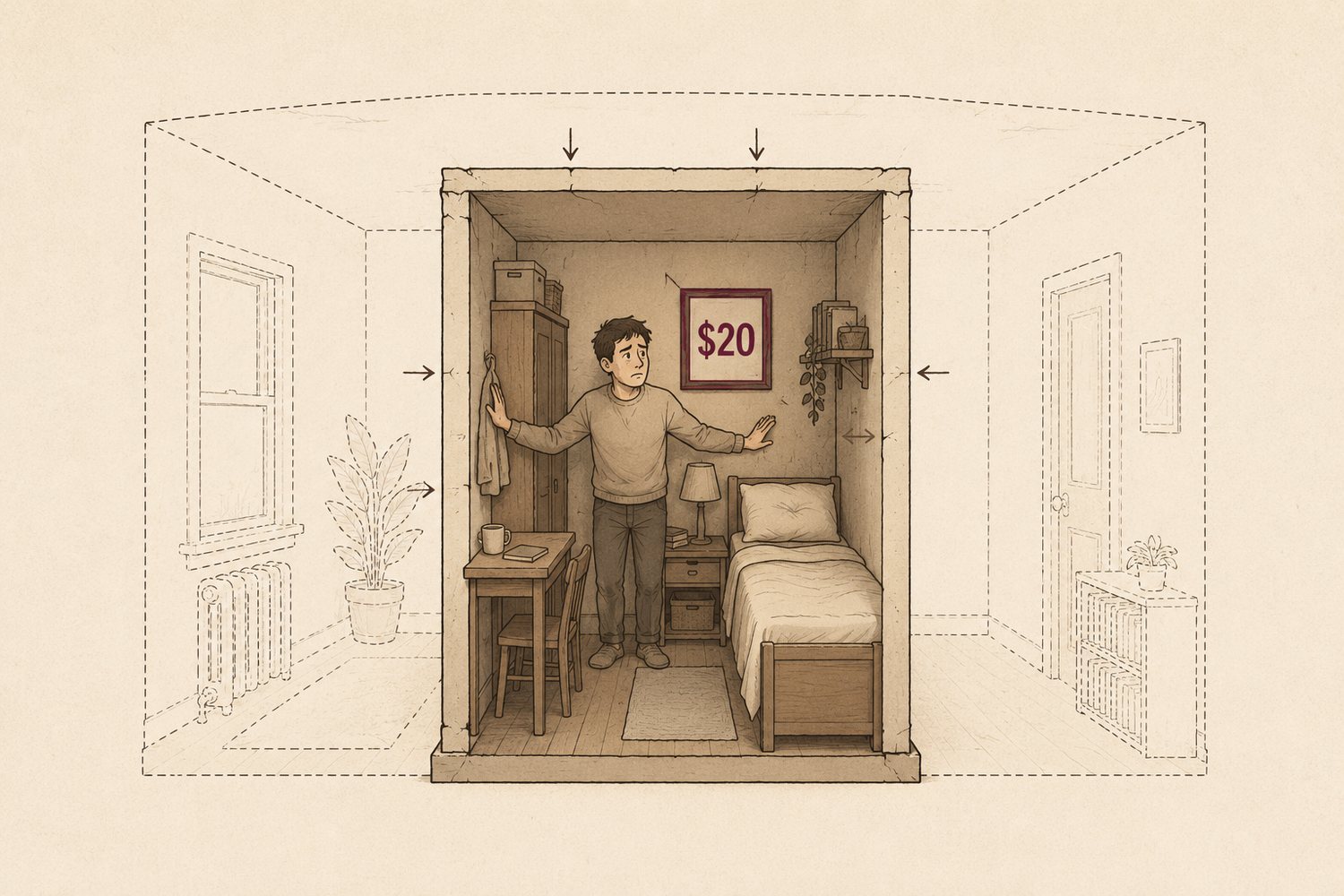

Imagine your landlord can't raise your rent — the number's fixed, printed, advertised to every prospective tenant. So instead they shrink the apartment. Same $2,000 a month, same lease, but the walls move in a foot a year. You're paying the old price for less of what you came for, and because the rent never changed, no rent-tracker, no tenant board, no spreadsheet will ever record an increase. That's not a metaphor I'm reaching for. It's the most common way AI software is raising prices right now, and it has a name: credit burn-rate repricing.

Across the AI Credit Index — 52 AI products read from their own pricing pages — this is the channel that does the most work while drawing the least attention. Outright sticker-price changes are the loudest move and the rarest. The quiet one is everywhere: hold the advertised price still, and change how fast it burns.

How the trick works

A credit-metered product has three numbers, and you only ever see one of them clearly.

The first is the plan price — $20 a month. Public, prominent, comparable. The second is the price per credit — often a reassuringly round “1 credit = 1 cent,” advertised right alongside. The third is the credit burn rate: how many credits a given action actually costs. That number is the one that does the damage, and it’s the one that lives where you can’t watch it — in a help doc, behind a per-model multiplier, on an in-app screen.

Hold the first two flat and move the third, and you have raised the price without raising a price. The pricing page is honest. The bill still goes up. And here’s the part that should bother any finance team: a fixed dollar price is not a fixed price. The whole apparatus of pricing discipline — competitive benchmarks, renewal reviews, procurement alerts — is built to watch the sticker. Credit burn-rate repricing is engineered, whether deliberately or by convenient accident, to be invisible to exactly that apparatus.

The pattern, four times

Once you know the shape, you see it repeat — same move, different products, all with the dollar figure held perfectly still.

Cursor. In January 2025, Cursor’s $20 Pro plan was generous: a few hundred fast requests plus unlimited slower ones, so the meter never really bit. In June 2025 the company reworked the plan around compute-and-dollar limits, stripped the unlimited fallback from the best models, and made paid overage the default — all while the headline stayed $20. The effective coverage roughly halved: the same money now bought something like half the usage it had. The backlash was fierce enough to force a public apology and refunds within weeks. The model survived intact. Same price, hardened meter.

GitHub Copilot. Copilot spent early 2025 as a flat seat — $10 a month, “unlimited” completions. It bolted on a “premium request” meter in April 2025, and then in 2026 re-based that meter again to bill on actual tokens consumed, one credit to the cent. Headline plan prices: unchanged. Reported effect on heavy agentic users: bills many times larger than before. The label “1 credit = 1¢” is doing reassurance work it hasn’t earned — pegging the dollar value of a credit tells you nothing about how many credits an action now eats.

monday.com. This one is almost too on-the-nose. As monday hardened its AI meter through late 2025, it cut the price per credit from roughly eight cents to one cent — a number that, read on its own, looks like a price decrease. In the same move it raised the cost of a standard AI action from 1 credit to 8. Eight credits at one cent is eight cents; one credit at eight cents was eight cents. The effective price per action didn’t move an inch — but “we lowered our per-credit price” is a sentence the company can now truthfully say. The cheaper-looking unit is the cover.

Make. In August 2025, Make renamed its billing unit from “operations” to “credits” at a clean 1:1, plan prices untouched. But the new credit consumes at variable, model-driven rates for AI-heavy steps — so an automation that leans on AI now drains the same dollar allowance faster than the identical-looking plan did a month earlier. A rename and a re-based consumption rate; not a cent of advertised change.

The list runs longer — Replit swapping flat per-checkpoint pricing for dynamic “effort-based” costs, Windsurf redefining its billing unit three times in eighteen months. The common thread never varies: the unit moves, the sticker doesn’t.

Why it’s spreading, and why it’s not (only) cynical

It would be too easy to file this purely as deception. The honest half of the story is that AI vendors have a real, variable cost under every action — the compute they pay for each model call — and a flat price asks them to eat that variance on their heaviest users. Re-basing the meter is, in part, a pass-through of a cost that genuinely moves. (That larger, more sympathetic story is its own essay: AI pricing is just COGS finally showing up.)

But that explains why the meter exists, not why the changes to it are so consistently routed around the visible price. A vendor passing through cost in good faith could simply raise the sticker and say why. The choice to hold the dollar figure still and move the hidden number is a choice about visibility — and it’s the same choice, made independently, by enough companies that it’s now a convention. It also fits the larger pattern in the Index: nearly every product has converged on the same metered model, and once your competitors all price the same way, the remaining lever is how quietly you can adjust it. (The convergence itself is the pillar essay.)

How to catch it

You catch a credit burn-rate reprice the way you’d catch the shrinking apartment: stop measuring the rent, start measuring the room.

- Track output per dollar, every quarter. How many generations, agent runs, or resolved tasks does your plan’s included allowance actually buy this quarter, versus last, at the same spend? That ratio is the real price. If it’s falling, you’ve been repriced — whatever the pricing page says.

- Treat a renamed unit as a yellow flag. “Operations” becoming “credits,” “requests” becoming “tokens,” “checkpoints” becoming “effort” — a unit change is the most common moment a credit burn rate gets re-based. Re-derive your cost-per-action the day it happens.

- Distrust a per-credit price cut. A lower price per credit, by itself, is meaningless and is sometimes the cover for a higher cost per action. Only the product of the two — dollars per unit of your work — counts.

- Get the credit burn rate into the contract. Plan price is easy to fix in writing; insist the credits-per-action schedule is too, or at least that material changes require notice. Most won’t offer it. The ones that do are telling you something.

None of this requires assuming bad faith. It just requires pricing the thing that actually moves. I’m logging these as they happen — dated, sourced, archived — in the Index’s change log, under their own category: a standing record of the price increases that were built to leave none. A static dollar price is not a static price. Watch the room, not the rent.

Related questions

- What is credit burn-rate repricing?

- It's a price increase that leaves the advertised price untouched. A credit-metered product raises what you actually pay by changing how many credits an action costs — the 'credit burn rate' — while the dollar figure on the pricing page, and often the price-per-credit, stays exactly the same. Your plan still says $20 and a credit still costs a cent, but the task that used to burn 1 credit now burns 8, so your real cost per unit of work quietly doubles or worse. The label holds still; the bill moves.

- Why don't price trackers catch AI credit burn-rate changes?

- Because every monitoring tool, procurement benchmark, and renewal review watches the dollar figure — and the dollar figure is exactly what these changes hold constant. A credit burn-rate reprice lives in the credits-per-action math and the per-model multipliers, which usually sit in help docs or in-app screens rather than on the pricing page. Nothing a crawler indexes changes, so nothing flags. You only notice when your monthly usage suddenly buys less than it did, which is to say after you've already paid more.

- How can I tell if an AI tool has raised its credit burn rate?

- Track output, not price. Each quarter, measure how much real work your plan's included credits actually buy — generations, agent runs, resolved tasks — and compare it to last quarter at the same dollar spend. If the same money buys meaningfully less, you've been repriced, regardless of what the pricing page says. Watch specifically for three tells: a unit being renamed (operations become 'credits'), a per-credit price being cut while the cost-per-action rises, and a shift to 'token-based' or 'effort-based' billing. All three are common covers for a credit burn-rate increase.